Show code

library(tidyverse)

library(scales)

library(arrow)

library(patchwork)

library(glue)This TidyTuesday builds the same six risk valuation matrices as the companion MakeoverMonday, using ggplot2: R-multiple vs required winrate, drawdown vs recovery rate, expectancy, losing streaks and capital loss, exponential growth, and consecutive-loss probability. Metrics are read from data/risk_metrics.parquet (generated by prepare_data.py).

library(tidyverse)

library(scales)

library(arrow)

library(patchwork)

library(glue)data_dir <- file.path(getwd(), "data")

risk_path <- file.path(data_dir, "risk_metrics.parquet")

if (file.exists(risk_path)) {

risk <- read_parquet(risk_path) %>% slice(1)

win_rate <- as.numeric(risk$win_rate_pct)

r_multiple <- as.numeric(risk$r_multiple)

max_dd <- as.numeric(risk$max_drawdown_pct)

max_streak <- as.integer(risk$max_consecutive_losing_days)

account_jpy <- as.numeric(risk$account_size_jpy)

pos_pct <- as.numeric(risk$position_size_pct)

cat("Loaded risk_metrics: WR =", win_rate, "%, R =", r_multiple, ", max DD =", max_dd, "%, max streak =", max_streak, "\n")

} else {

win_rate <- 55; r_multiple <- 1.5; max_dd <- 10; max_streak <- 3

account_jpy <- 1e7; pos_pct <- 2

cat("Using default risk metrics (run prepare_data.py to use your data)\n")

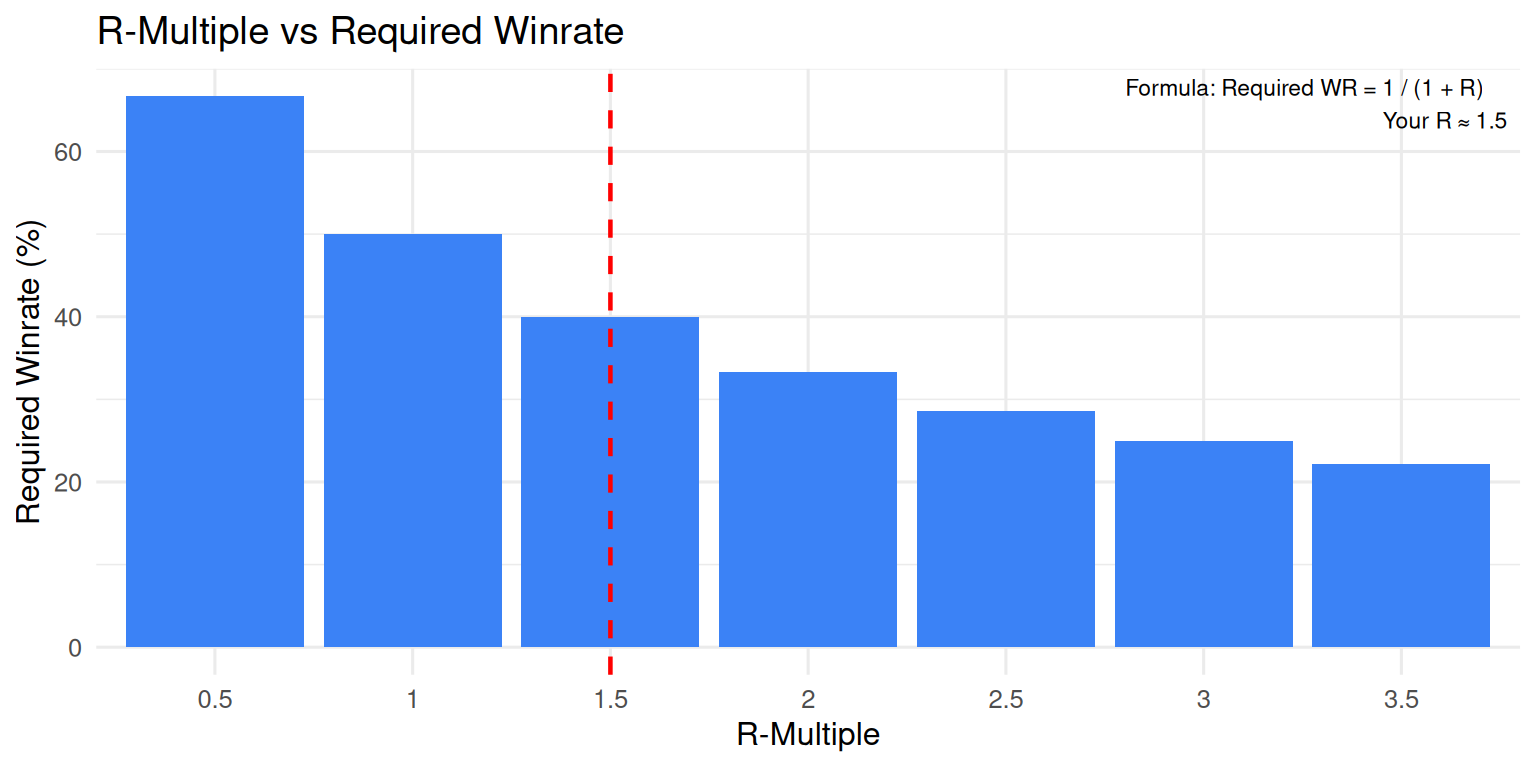

}Loaded risk_metrics: WR = 55 %, R = 1.5 , max DD = 0 %, max streak = 0 r_vals <- seq(0.5, 3.5, by = 0.5)

req_wr <- 100 / (1 + r_vals)

tbl1 <- tibble(r_multiple = r_vals, required_winrate_pct = req_wr)

p1 <- ggplot(tbl1, aes(x = factor(r_multiple), y = required_winrate_pct)) +

geom_col(fill = "#3b82f6") +

geom_vline(xintercept = which.min(abs(r_vals - r_multiple)), linetype = "dashed", color = "red", linewidth = 0.8) +

annotate("text", x = Inf, y = Inf, label = glue("Formula: Required WR = 1 / (1 + R)\nYour R ≈ {round(r_multiple, 2)}"), hjust = 1.1, vjust = 1.2, size = 3) +

labs(title = "R-Multiple vs Required Winrate", x = "R-Multiple", y = "Required Winrate (%)") +

theme_minimal(base_size = 12)

p1

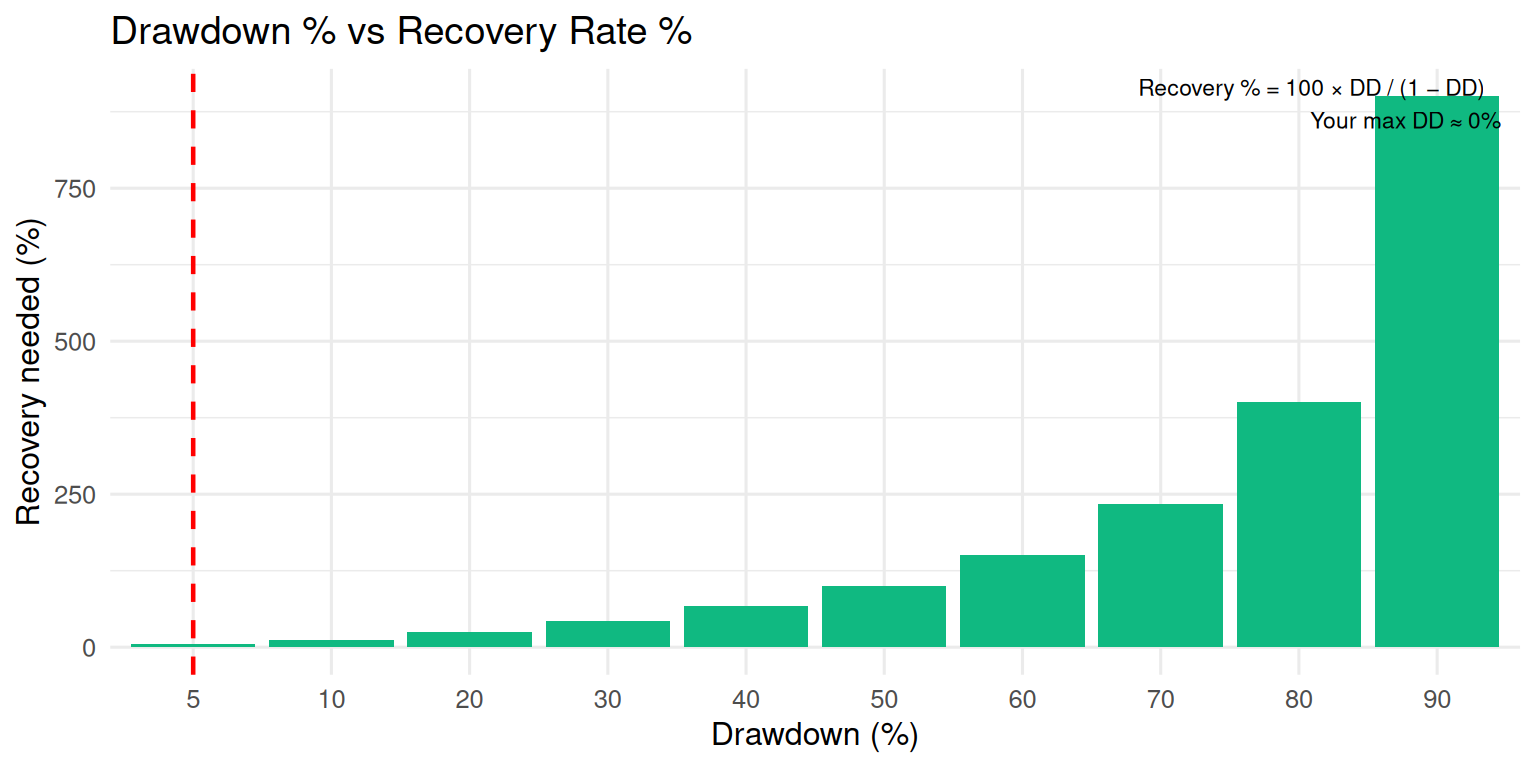

dd_pcts <- c(5, 10, 20, 30, 40, 50, 60, 70, 80, 90)

recovery <- 100 * dd_pcts / (100 - dd_pcts)

tbl2 <- tibble(drawdown_pct = dd_pcts, recovery_pct = recovery)

p2 <- ggplot(tbl2, aes(x = factor(drawdown_pct), y = recovery_pct)) +

geom_col(fill = "#10b981") +

geom_vline(xintercept = which.min(abs(dd_pcts - max_dd)), linetype = "dashed", color = "red", linewidth = 0.8) +

annotate("text", x = Inf, y = Inf, label = glue("Recovery % = 100 × DD / (1 − DD)\nYour max DD ≈ {round(max_dd, 0)}%"), hjust = 1.1, vjust = 1.2, size = 3) +

labs(title = "Drawdown % vs Recovery Rate %", x = "Drawdown (%)", y = "Recovery needed (%)") +

theme_minimal(base_size = 12)

p2

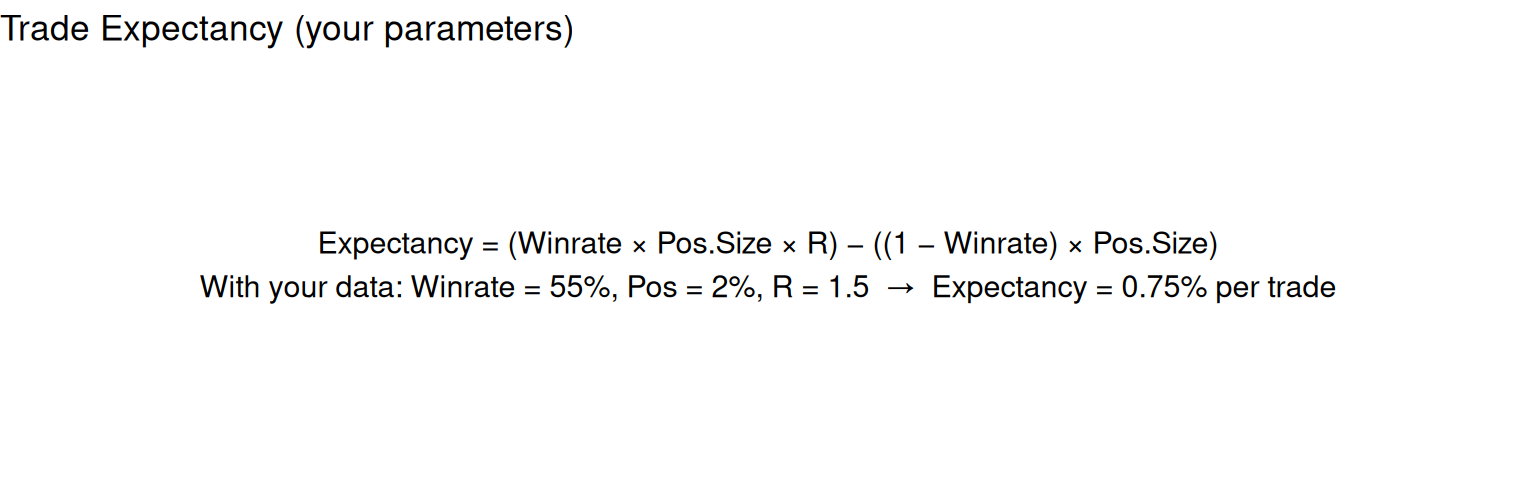

wr_dec <- win_rate / 100

exp_pct <- (wr_dec * pos_pct * r_multiple) - ((1 - wr_dec) * pos_pct)

p3 <- ggplot() +

annotate("text", x = 0.5, y = 0.5, label = glue(

"Expectancy = (Winrate × Pos.Size × R) − ((1 − Winrate) × Pos.Size)\n",

"With your data: Winrate = {win_rate}%, Pos = {pos_pct}%, R = {round(r_multiple, 2)} → Expectancy = {round(exp_pct, 2)}% per trade"

), size = 4, hjust = 0.5, vjust = 0.5) +

scale_x_continuous(limits = c(0, 1)) +

scale_y_continuous(limits = c(0, 1)) +

labs(title = "Trade Expectancy (your parameters)") +

theme_void()

p3

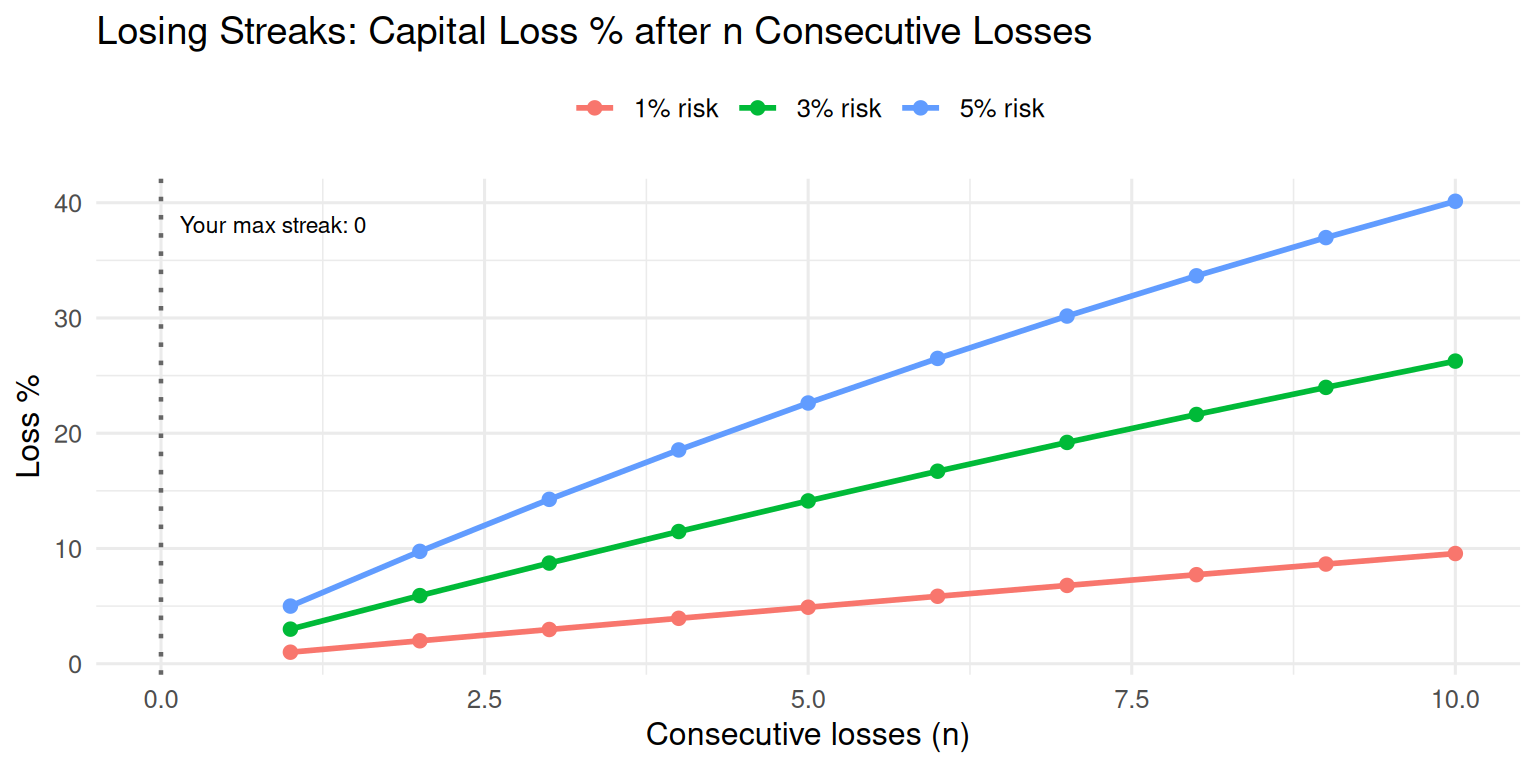

n_losses <- 1:10

risks <- c(0.01, 0.03, 0.05)

tbl4 <- expand_grid(n = n_losses, risk_pct = risks) %>%

mutate(loss_pct = 100 * (1 - (1 - risk_pct)^n), risk_lab = paste0(risk_pct * 100, "% risk"))

p4 <- ggplot(tbl4, aes(x = n, y = loss_pct, color = risk_lab)) +

geom_line(linewidth = 1) +

geom_point(size = 2) +

geom_vline(xintercept = max_streak, linetype = "dotted", color = "gray40", linewidth = 0.8) +

annotate("text", x = max_streak, y = max(tbl4$loss_pct) * 0.95, label = glue("Your max streak: {max_streak}"), hjust = -0.1, size = 3) +

labs(title = "Losing Streaks: Capital Loss % after n Consecutive Losses", x = "Consecutive losses (n)", y = "Loss %", color = NULL) +

theme_minimal(base_size = 12) +

theme(legend.position = "top")

p4

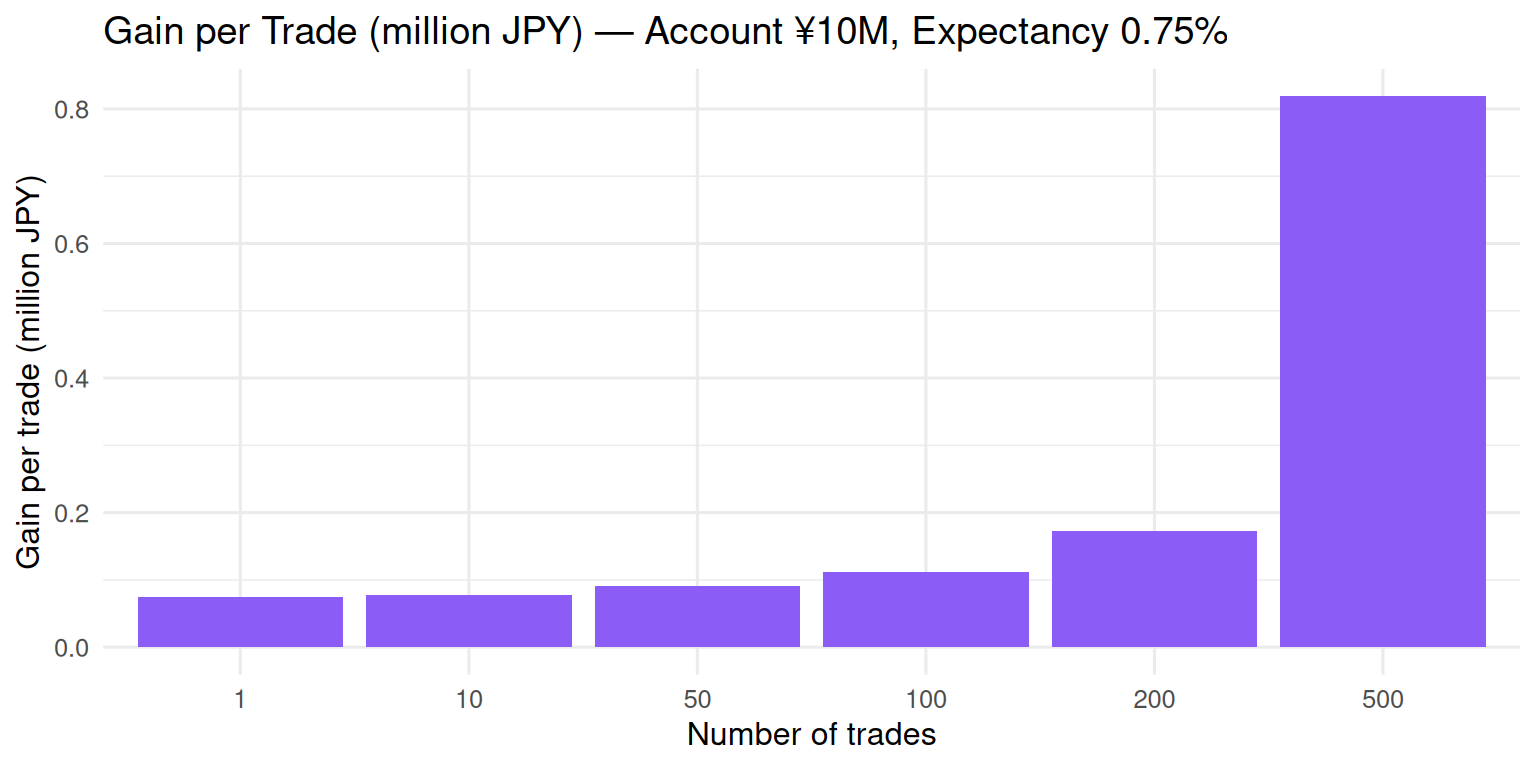

E <- exp_pct / 100

account_0 <- if (account_jpy > 0) account_jpy else 1e7

account_m <- round(account_0 / 1e6, 1)

n_trades <- c(1, 10, 50, 100, 200, 500)

gain_per <- account_0 * ((1 + E)^n_trades - 1) / n_trades

tbl5 <- tibble(n_trades = factor(n_trades), gain_million_jpy = gain_per / 1e6)

p5 <- ggplot(tbl5, aes(x = n_trades, y = gain_million_jpy)) +

geom_col(fill = "#8b5cf6") +

labs(

title = glue("Gain per Trade (million JPY) — Account ¥{account_m}M, Expectancy {round(exp_pct, 2)}%"),

x = "Number of trades", y = "Gain per trade (million JPY)"

) +

theme_minimal(base_size = 12)

p5

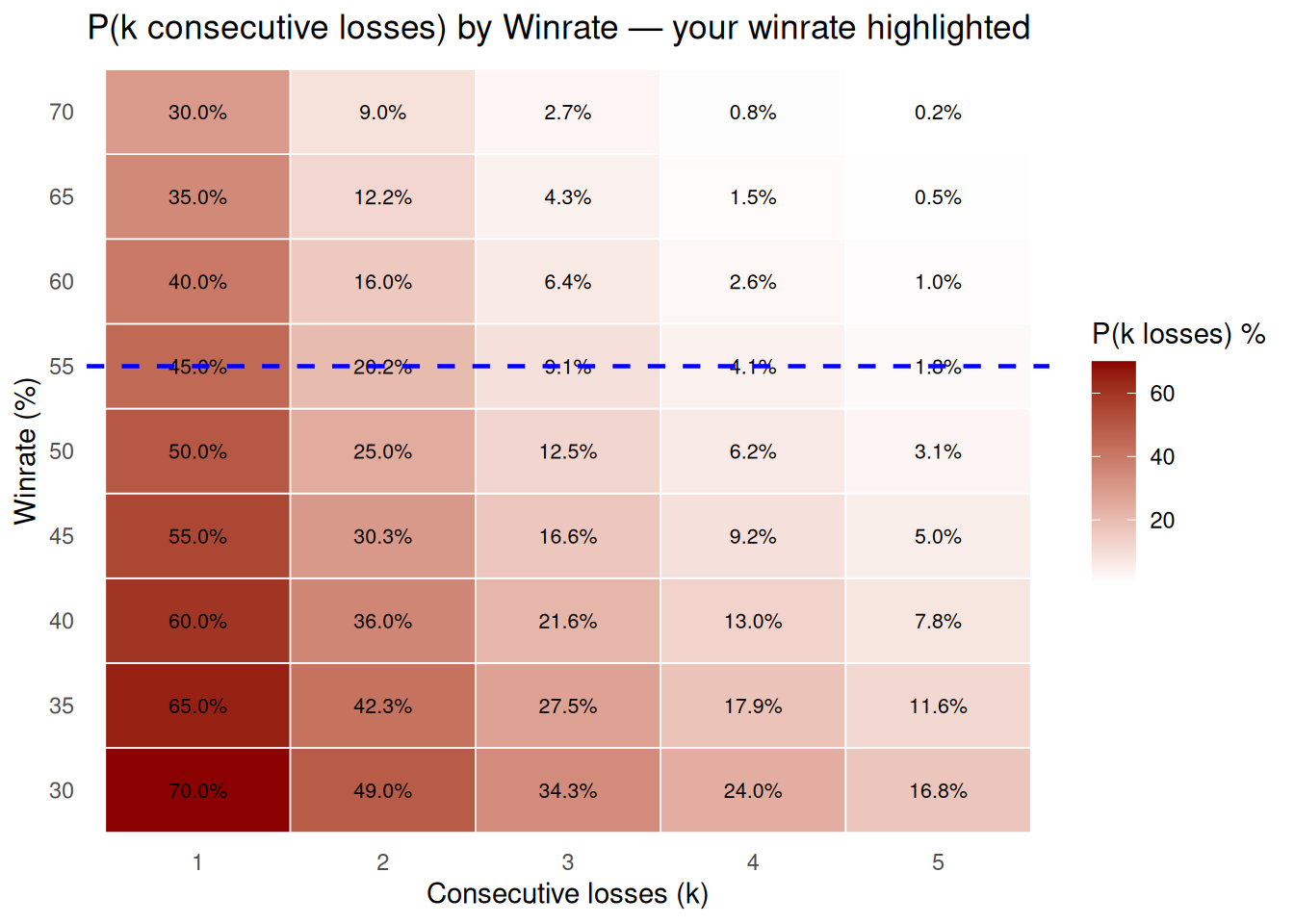

winrates <- seq(30, 70, by = 5)

k_streaks <- 1:5

tbl6 <- expand_grid(winrate_pct = winrates, k = k_streaks) %>%

mutate(prob_pct = 100 * (1 - winrate_pct/100)^k)

p6 <- ggplot(tbl6, aes(x = factor(k), y = factor(winrate_pct), fill = prob_pct)) +

geom_tile(color = "white", linewidth = 0.3) +

geom_text(aes(label = sprintf("%.1f%%", prob_pct)), size = 2.8) +

scale_fill_gradient(low = "white", high = "darkred", name = "P(k losses) %") +

geom_hline(yintercept = which.min(abs(winrates - win_rate)), linetype = "dashed", color = "blue", linewidth = 0.8) +

labs(

title = "P(k consecutive losses) by Winrate — your winrate highlighted",

x = "Consecutive losses (k)", y = "Winrate (%)"

) +

theme_minimal(base_size = 11) +

theme(panel.grid = element_blank())

p6

This post is part of the TidyTuesday weekly data visualization project.